Report released by NYPPEX on February 6, 2026 in Miami, FL United States.

Purpose

This report provides a detailed examination of secondary market pricing dynamics for interests in private credit funds during the second half of 2025, based on NYPPEX’s proprietary estimates and analysis of market data. It highlights the impact of heightened investor scrutiny on underlying loan quality and key credit metrics.

Executive Summary

In the second half of 2025, secondary bid prices for private credit fund interests exhibited notable dispersion, ranging from 82.50% to 98.75% of net asset value (NAV). This widening range reflects increased investor caution amid economic pressures, rising defaults in certain sectors, and greater emphasis on portfolio risk assessment. Buyers prioritized transparency into loan-level metrics, resulting in more differentiated pricing compared to prior periods.

The private credit asset class continues to mature, with secondary participants applying rigorous due diligence to indicators such as payment-in-kind (PIK) ratios, interest coverage, and default exposure. This shift has led to pricing that more closely aligns with perceived underlying credit quality.

NYPPEX’s estimates draw from proprietary modeling, publicly available data sources (including Fitch Ratings and Bank of America reports), and market observations. These insights serve as liquidity benchmarks for institutional investors and fund managers.

Key Trends in Private Credit for the Second Half of 2025

NYPPEX’s comprehensive review draws from proprietary analysis of publicly available data, market estimates, and industry benchmarks. Below are the primary trends observed:

- PIK to Income Ratios Averaged 7.3% in 2025

- Corporate Loan Quality Weakened in 2025

- Corporate Bankruptcy Filings Increased 7% in December 2025

- Net Asset Values Increased 9% in 2025

The following sections provide a detailed breakdown of each of these key trends, highlighting their underlying drivers and potential implications for the private credit market.

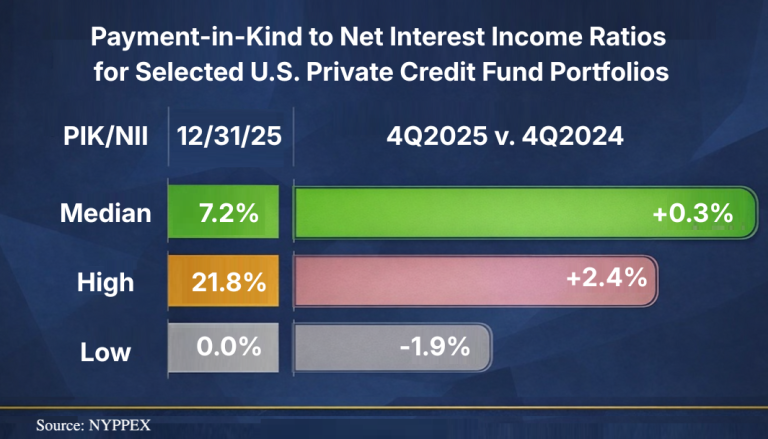

Rising PIK to Income Ratios Signal Borrower Stress

One notable indicator of potential distress in private credit portfolios is the PIK to income ratio, which measures the proportion of interest payments deferred as payment-in-kind rather than paid in cash. In the second half of 2025, this ratio averaged 7.3% across U.S. private credit funds, with significant variation from 0% to as high as 21%. Quarter-over-quarter in Q4 2025, the average PIK ratio rose by about 0.4%, though individual funds experienced changes ranging from an increase of 2.5% to a decrease of 1.9%. Elevated PIK levels often indicate that borrowers are under financial pressure, opting to defer payments to conserve cash amid higher interest rates and operational challenges. This metric is particularly watched by secondary investors, as it can foreshadow higher default risks and impact overall fund performance. Earlier NYPPEX in its 2025 Midyear Outlook projected distributions from private equity to remain at historical lows of 9% of NAV.

Mixed Signals in Corporate Loan Quality

Data from Fitch Ratings and Bank of America paints a picture of deteriorating credit conditions in certain segments of the market. Default rates in stressed sectors climbed to around 6% during this period, driven by factors like supply chain disruptions, inflationary pressures, and geopolitical tensions. However, senior direct lending portfolios—often prioritized for their secured status—maintained default rates below 2%, offering some stability. A key concern is the decline in interest coverage ratios, which measure a borrower’s ability to meet interest obligations from earnings. These ratios fell to an estimated 1.5x in the second half of 2025, down sharply from 3.2x in 2021. This erosion highlights reduced resilience among corporate borrowers, making them more susceptible to prolonged economic slowdowns or unexpected shocks.

Surge in Bankruptcy Trends

Corporate distress has manifested in rising bankruptcy filings across the U.S. In December 2025 alone, filings increased by 7% compared to the previous year, contributing to an overall 5% rise for the full year—from 30,201 in 2024 to 31,810 in 2025. The peak of this wave occurred in late 2024 and early 2025, with mid-sized companies (those with EBITDA between $25-49 million) experiencing the most acute pressures. Default rates in this segment moderated from 4-5% earlier in the year to 2-2.5% by Q3 2025, but the uptick in bankruptcies underscores ongoing vulnerabilities. Sectors like retail, energy, and manufacturing have been hit hardest, prompting secondary buyers to favor funds with diversified portfolios and stronger risk mitigation strategies.

Varied NAV Performance Across Funds

Despite these headwinds, private credit fund NAVs showed resilience on average, with a 9.2% year-over-year increase in 2025. However, performance was far from uniform, with individual funds ranging from a decline of 14% to gains of up to 24%. A common thread among higher-performing funds was a heavy allocation to first-lien loans, which averaged 83% of portfolios (ranging from 48% to 97%). These loans, typically floating-rate and senior secured, provide a buffer against interest rate volatility and offer better recovery rates in defaults. Funds with greater exposure to subordinated or riskier debt structures faced more downward pressure on NAVs.

Outlook for 2026: Responsiveness to Loan Quality Remains Key

As we move into 2026, NYPPEX expects secondary prices to continue reflecting real-time assessments of loan quality. Buyers are likely to prioritize funds with robust credit metrics, low PIK exposure, and minimal default risks, potentially leading to even wider price dispersions if economic conditions worsen. Factors such as interest rate trajectories, inflation trends, and global events will play a critical role in shaping market dynamics. Institutional investors and fund managers should monitor these indicators closely to navigate liquidity challenges and optimize secondary market opportunities, particularly as the growing impact of emerging technologies and AI on financial markets continues to reshape investor decision-making trend.

NYPPEX’s insights are derived from a blend of proprietary methodologies, public data sources, and market intelligence, serving as essential benchmarks for liquidity in private capital. This analysis is tailored for U.S. Qualified Purchasers under the Securities Act of 1933, with non-U.S. investors advised to review local regulations.

About NYPPEX

NYPPEX is a pioneer in secondary market price data for interests in private capital funds. Its core subscription-based service is to provide quarterly secondary price estimates on portfolios of interests in private capital funds. Since 2004, its QMS has been recognized by an IRS private letter ruling, providing a safe-harbor exemption under U.S. Treasury Regulation §1.7704-1 to help funds maintain tax compliance when permitting secondary interest transfers. This market commentary is intended for U.S. Qualified Purchasers as defined under the Securities Act of 1933. Non-U.S. investors should consult local regulations. NYPPEX is not a broker-dealer and does not solicit securities transactions. © 2026 NYPPEX Holdings, LLC. All rights reserved.

For more information, contact Rich Martin at rmartin@nyppex.com.

Disclaimer

The information in this market commentary is for educational and informational purposes only and does not constitute investment, legal, or tax advice. The information contains forward- looking statements that involve numerous risks and uncertainties. Actual results may differ. Data contained herein is estimated and obtained from what we consider to be reliable sources; however, it is incomplete, and our information may change without further notice. We are not a broker dealer. Nothing in this commentary is a solicitation of any securities transactions.